Market Shift: Home inventory in the Twin Cities approaches a 5-year high while pending sales fall to a 15-year low amidst higher interest rate regime

(Data Sources: You can track Twin Cities housing market trends here. You can track mortgage rates here. You can track home builder confidence here. You can track lumber prices here. You can track showing volume here.)

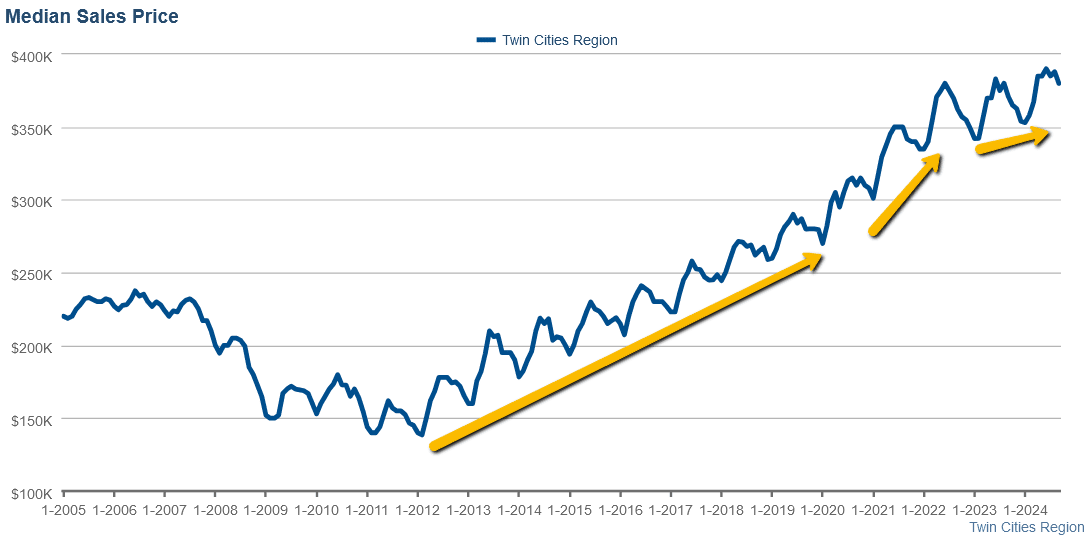

Amidst the "higher for longer" interest rate regime, housing markets, both locally and nationally, continue to shift from extreme, pandemic fueled, inflationary markets, to softer, more neutral markets, and in some cases (SW Florida for example), are starting to tilt towards buyers. The Twin Cities is not immune to this and has been clearly shifting over the past two years to a softer market as the median home price is up only 2.4% YOY and only 4.9% since September of 2022, with much of that inflation happening at the lower end/starter home segment of the market.

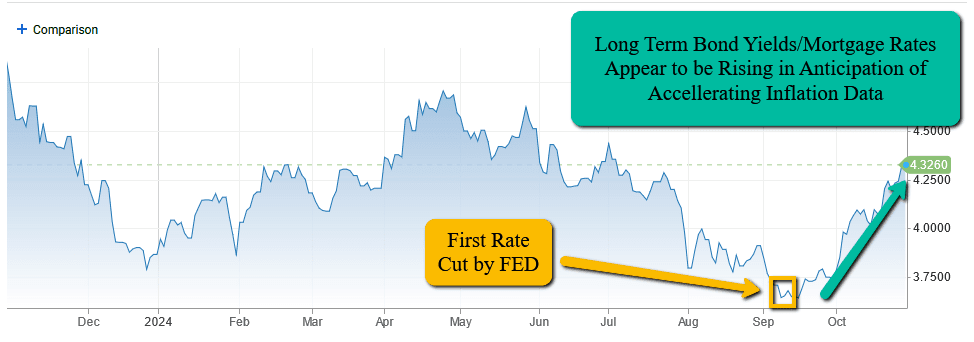

Mortgage Rates: Consensus belief heading into 2024 was that inflation was largely vanquished and that mortgage rates would begin to head back toward pre-pandemic levels in the 4 - 5% range, which has not been the case. Additionally, there appears to be a misconception in the public regarding the relationship between the moves in the federal funds rate, and mortgage rate moves in that many people seem to believe that there is a direct relationship, which is not true, the relationship is indirect and anticipated. Mortgage-backed securities are long term debt that trade in the bond market. The three primary factors that impact bond yields are relative growth, inflation, and Fed policy. The bond market uses evolving inflation data, growth data and Fed sentiment, to anticipate Federal Reserve moves and often, by the time the Fed takes action, that action is already reflected within the mortgage rates via the bond market’s anticipation of those moves.

Mortgage rates have cooled significantly since their cycle highs in the 8% range, from October of '23, however our economic advisor (Hedgeye Risk Management) has had inflation accelerating more than expected, starting in Q4 of '24 (starting around October 1) and lasting at least through Q2 of '25, so we believe the immediate cycle lows for mortgage rates are behind us and we are anticipating more upside risk to bond yield/mortgages rates, than downside potential, at least through the first half of '25. Since the Fed cut rates last month, the average 30-Year-Fixed mortgage rate in the U.S. has ripped upwards from 6% back to almost 7%.

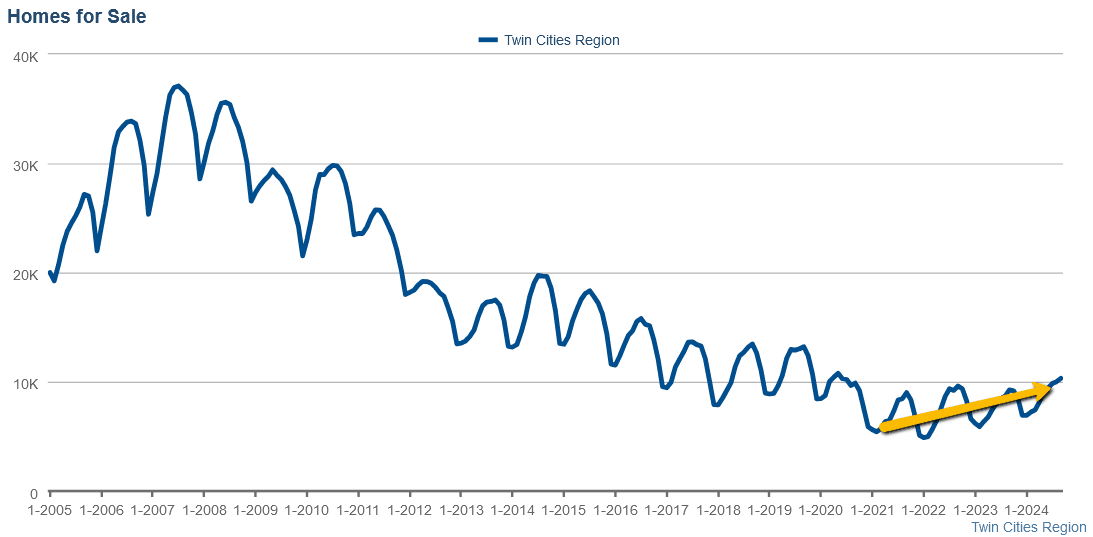

Home Inventory: Home inventory in the Twin Cities, not including shadow inventory like available lots in new construction developments, has moved back above 10,000 units for the first time since the onset of the pandemic (10,357 active listings of homes, condos, lofts). This is likely at or near the seasonal peak as inventory tends to decline ruing the latter part of fall and through the winter, typically bottoming sometime during the month of January.

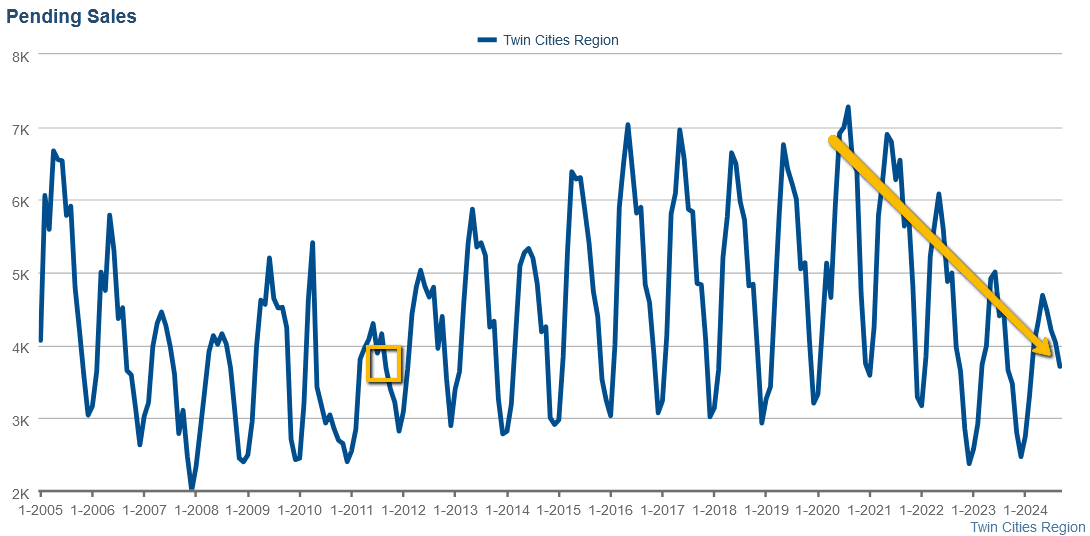

Pending Home Sales: Pending home sales in the Twin Cities fell 8% in September to 3,719 units. This represents the lowest # of pending sales during the month of September since 2011, the height of the 2008 financial and foreclosure crisis, and a 13-year low. We expect pending sales volume to continue to decline until forming a bottom at some point in December and then to accelerate again starting in January.

The Median Home Price: The median home price in the Twin Cities continued its seasonal decline in September but remains up a marginal 1.6%, YOY, as we continue to shift towards neutral.

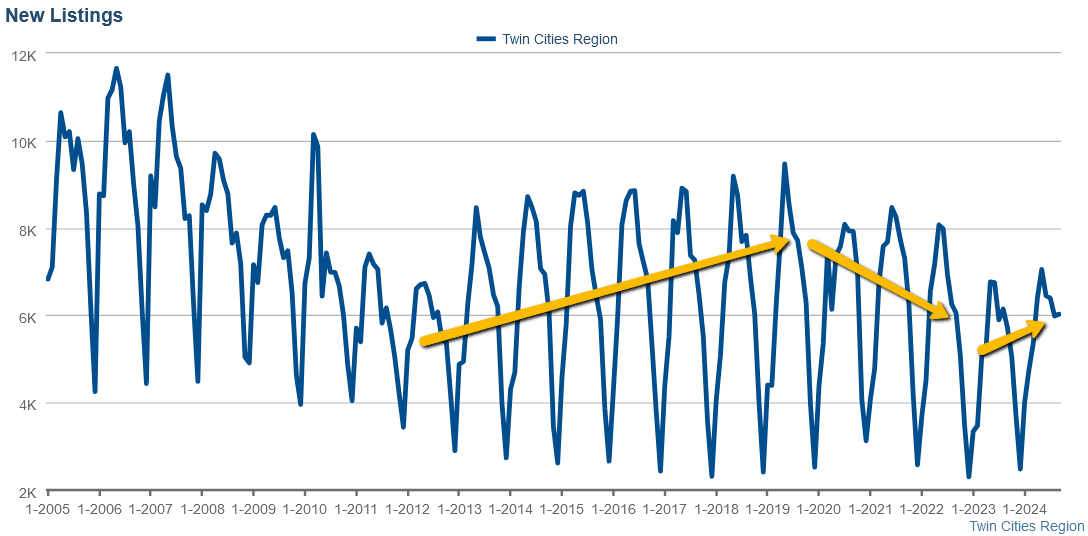

New Listings: In September, new listing volume in the Twin Cities continued its acceleration from the lows of 2023, inspired by the dynamic of consumers being "married to their mortgage rates", caused by the higher for longer interest rate regime. This appears to be be inspired by 1) the correction in interest rates from 8% down to 6%, 2) a general shift in the desire to own multiple homes, land, etc, and 3) with the idea that people can only stay married to their mortgage so long as their home needs do not urgently change, but eventually, people have to sell or move so I think there is some pent up selling happening.

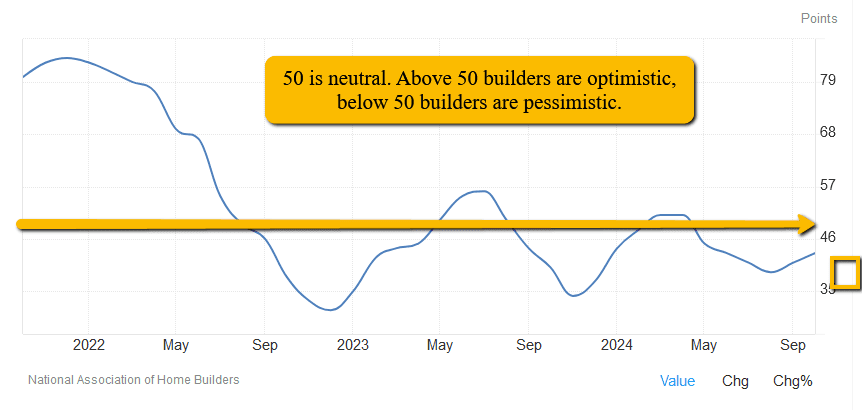

Homebuilder Sentiment: "The NAHB/Wells Fargo Housing Market Index in the US rose to 43 in October of 2024 from 41 in the previous month, the highest since June, and slightly ahead of market expectations of 42. The gauge for current sales conditions rose by 2 points to 47, while sales expectations in the upcoming 6 months rose by a sharper 4 points to 57, supported by expectations that rate cuts by the Fed would stimulate housing demand. Accordingly, the gauge measuring traffic of prospective buyers rose by 2 points to 29. In the meantime, the share of builders that are cutting prices was loosely unchanged from the prior month at 32%."

It is our current belief that the narrative which spurred the increase in builder sentiment in October will play out bearishly for builder confidence as we believe (Source: Hedgeye Risk Management) that inflation has begun to accelerate and will likely continue to accelerate through Q2 of 2025. If that turns out to be true, it will likely continue to put or keep upward pressure on rates through the first part of 2025.

This concludes our Twin Cities housing market insight for October of 2024. Please don't hesitate to call us at 952-222-SOLD if you would like to go more in depth on a particular market segment or dive into the current fair market value of a property that you currently own or manage.

Sources: NorthstarMLS, Infosparks Data, Hedgeeye Risk Management, FreddieMac.com, Nasdaq.com, TradingEconomics.com, fred.stlouisfed.org, The National Association of Home Builders