BARRING MACRO ECONOMIC & GEOPOLITICAL RISKS, HOUSING IS POISED FOR ITS STRONGEST SPRING SINCE 2022

Author:

Data Sources: You can track Twin Cities housing market trends here. You can track mortgage rates here. You can track home builder confidence here. You can track lumber prices here. You can track the economic policy uncertainty index here. You can track gold prices here and silver prices here. You can track showing volume here.

In 2025, the median home price in the Twin Cities for closed sales during the month of May fell. If you go back over 50 years of data, there is only one other year where home prices did not increase significantly for closed sales in May, let alone decline, which was during the onset of the Covid-19 pandemic in the spring of 2020. During the other 48 years, the median home price moved up in May.

The spring market of 2025 began mostly as expected with stabilization in January, a 12-month low in inventory, demand accelerating, and prices starting to move back up from their winter lows. However, a major headwind materialized and helped to make the 2025 spring market one of the rockiest, most challenging spring markets on record, especially for the upper bracket price points, record uncertainty about US trade policy.

2025 Spring Market Headwinds:

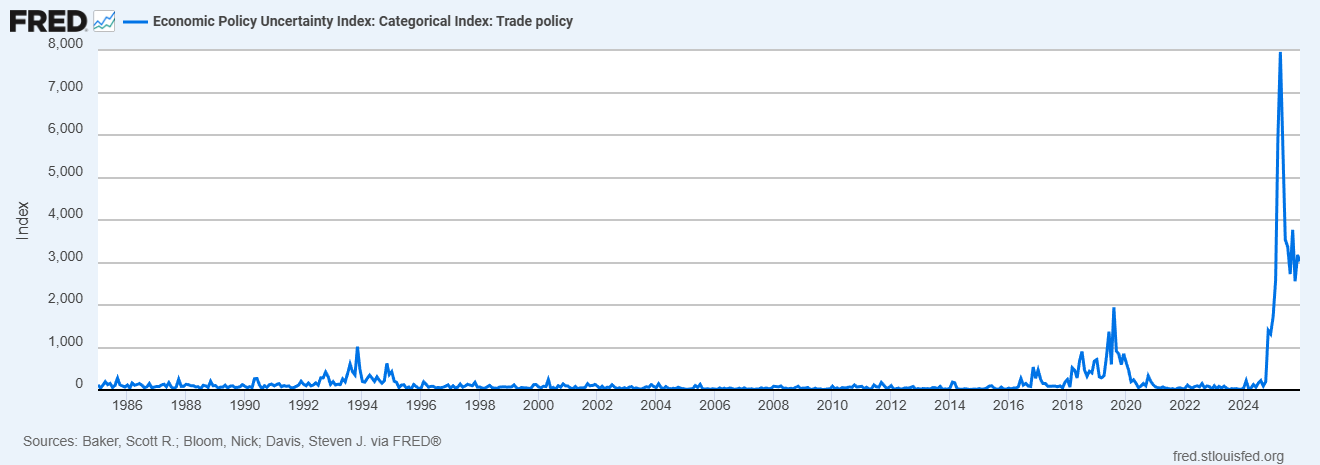

- Trade Policy Uncertainty: After the election of Donald Trump, economic trade policy uncertainty as measured by the EPUTRADE index (see chart below) started rising. After the inauguration, the uncertainty moved up to a record high, then proceeded to go parabolic (to 4X the previous record high in April before cooling off into the summer). This had a similar “gridlock” effect to the early stages of the pandemic where paralyzing uncertainty caused a pause for many folks on the demand side.

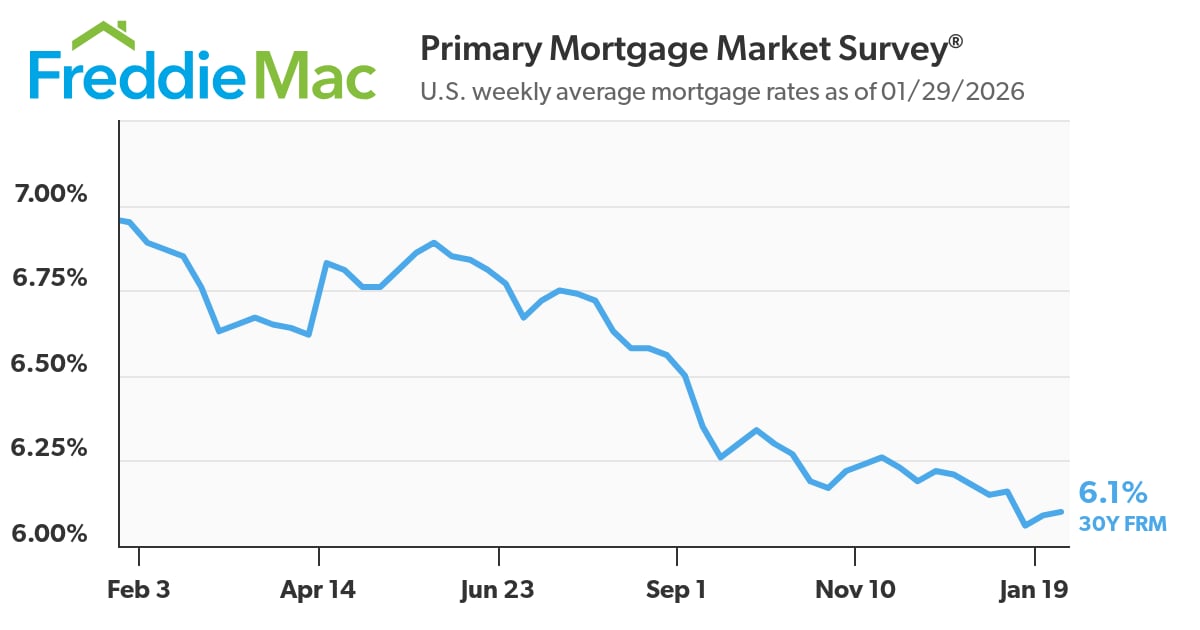

- Mortgage Rates: Rates were also a headwind for the 2025 spring. We started off 2025 with mortgage rates at 7% and they held a 6.5% - 7.2% trading range until late summer when they finally fell below 6.5% and then continued to decline as the latter part of the year progressed.

Contrast with the start of the 2026 Spring Market:

- Trade Policy Uncertainty: Economic policy uncertainty remains a headwind for the housing market at more than 30% above previous record highs which does have an impact on consumer confidence, especially in the upper bracket housing markets, but is down more than 60% since the April of 2025 peak and is much less volatile heading into the spring market.

- Mortgage Rates: Rates are still double where they were during the easy money days of the pandemic, but we started off 2026 with mortgage rates in the low 6% range, down 12% YOY, which gives a significant boost to affordability via a lower cost of capital as compared to where we were during the spring of 2025.

Economic Policy Uncertainty Index Chart:

Geopolitical Risks: The United States is currently involved in numerous military, economic, trade, and resource related conflicts on all sides of the globe, any of which could evolve into something that could have more impact on the domestic economy, and therefore the housing market. This is just something to keep an eye on.

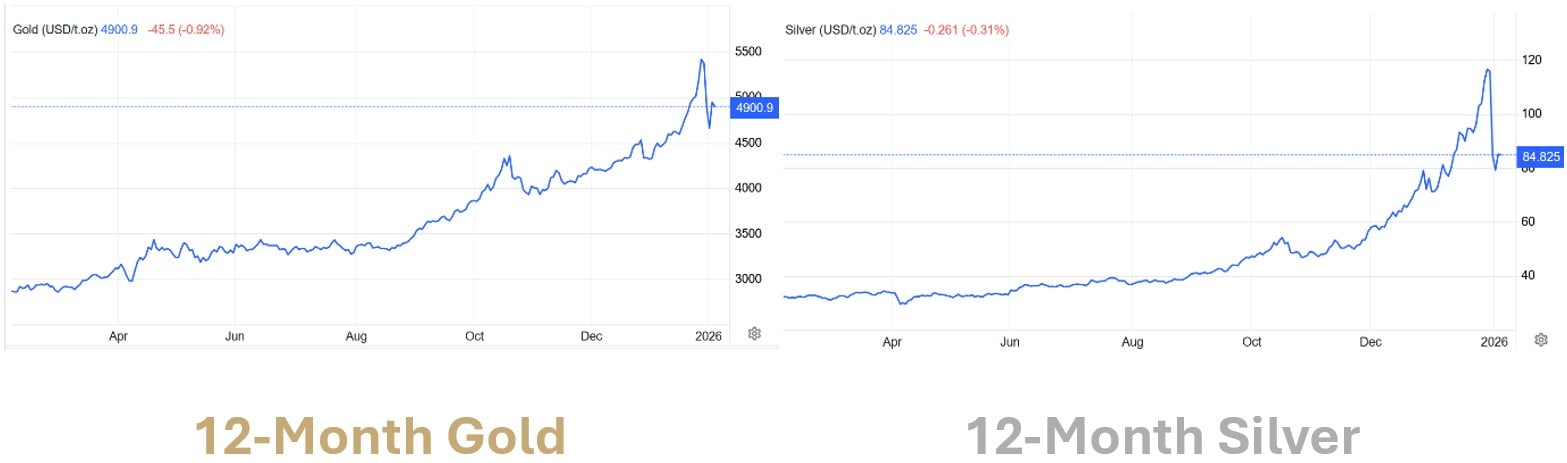

Monetary Metals Are Signaling Macro Risk / Opportunity: Gold and silver moved up a massive +64% (gold) and +163% (silver) respectively in 2025. The last two occasions where gold and silver (which tend to be much less volatile) moved like this in USD terms, was during 2005 - 2007 which signaled the 2008 financial crisis and the great recession / easy money era that followed, and then twice during the 1970s in response to runaway inflation which signaled the 'Ronald Reagan/Paul Voelker' tight money era along with the financial crisis and recession that followed from 1980 - 1981. We don't know what exactly what is being signaled this time, but these historical moves serve as a reminder that 1) there are some structural debt, macro, and geopolitical risks/opportunities out there to be considered when undertaking any major financial decisions, and 2) priced in gold/silver (which has served as money across the entire planet for more than 5,000+ years) most financial assets, including housing, have not actually increased in value, but rather it us our currency that has been steadily falling in its purchasing power.

2026 Spring Market Expectations: There is a heightened level of macro-economic and geopolitical risk out there that could cause things to change quickly, however, provided those risks remain at bay, with home inventory down slightly YOY and with some of the major market headwinds down YOY and subsiding, with regards to home price appreciation in the Twin Cities and across the country, I expect the 2026 spring market to be the strongest since 2022.

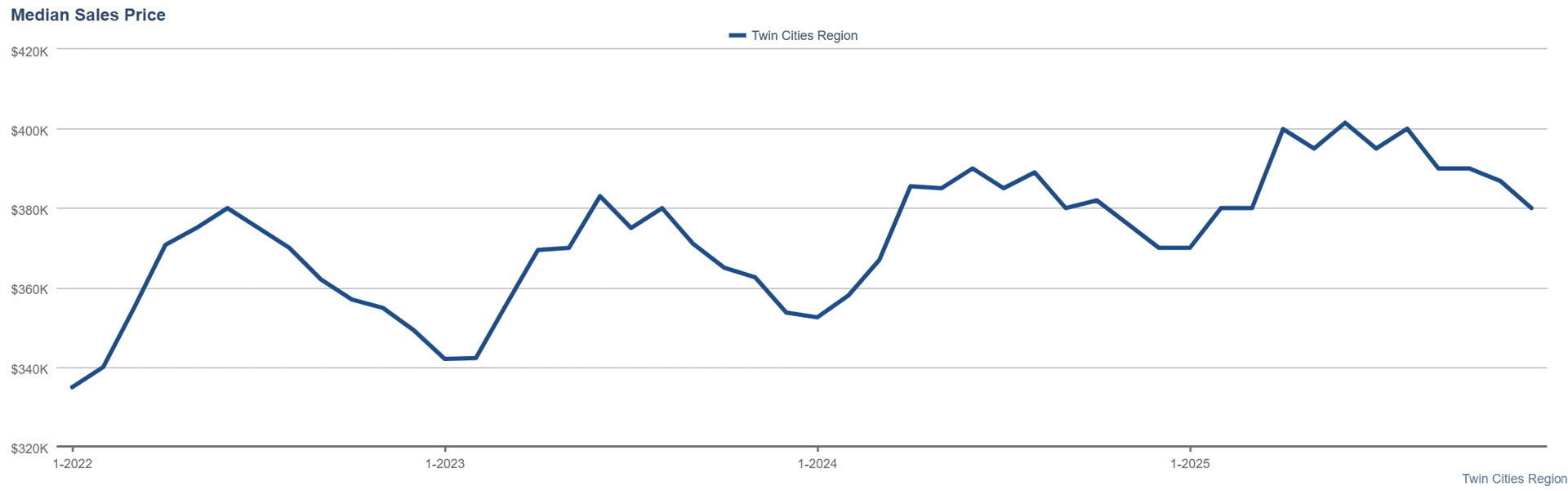

The Median Home Price: The median sales in the Twin Cities (all home types) for December landed at $380,000. This is down 1.75% MOM and up 2.7% YOY, as expected and in line with the seasonal cycle.

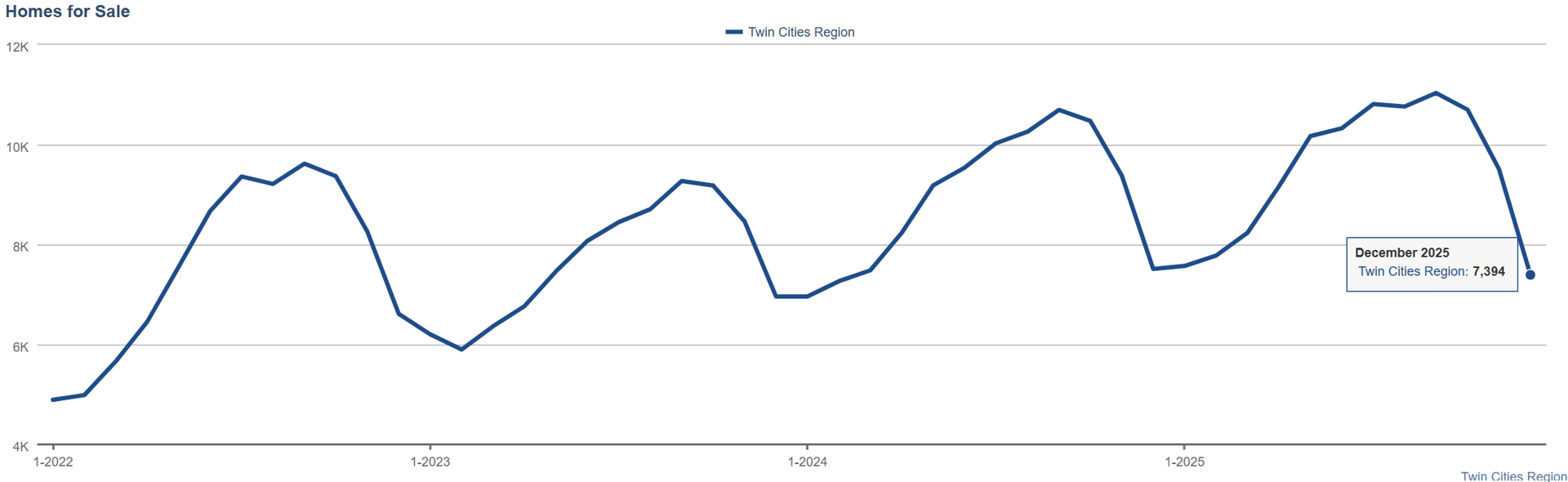

Home Inventory: Inventory in the Twin Cities ended the year at 7,394 units (Homes, Condos, Townhouses), down 22% MOM and down 1.57% year over year, as expected and in line with the seasonal cycle.

Mortgage Rates: Mortgage rates have been trending down since May of 2025. 30-year interest rates in the last week of January averaged 6.1, down slightly from the previous month, and down over 12% from the same time last year when interest rates were hovering around 7%.

Sources: NorthstarMLS, InfoSparks Data, Hedgeeye Risk Management, FreddieMac.com, Nasdaq.com, TradingEconomics.com, fred.stlouisfed.org, The National Association of Home Builders