You can track the Twin Cities housing market data here. You can track mortgage rates here. You can track homebuilder confidence here. You can track showing activity here. You can track lumber prices here.

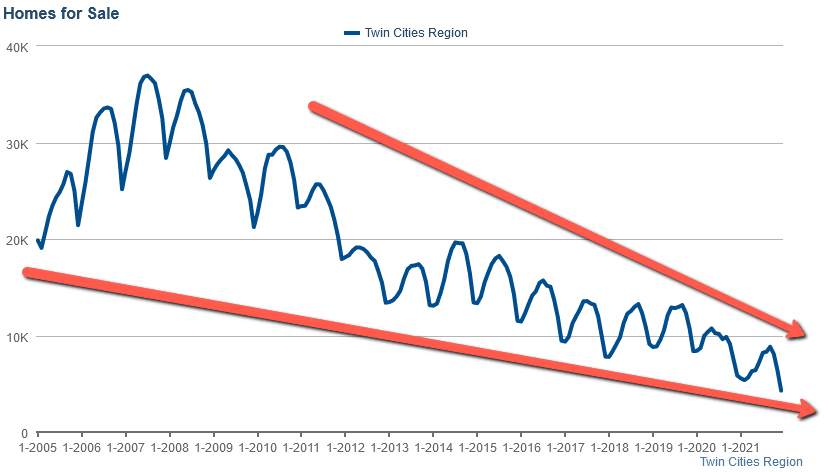

Home inventory in the Twin Cities fell 32% in December to 4,287 units (homes, condos, lofts & townhouses), a new all-time low and 20% below the previous record of 5,378 units from December of 2021. This will no doubt set the stage for another bidding-war-filled spring market as the seasonal rise in demand finds a worse inventory shortage than it found in 2021.

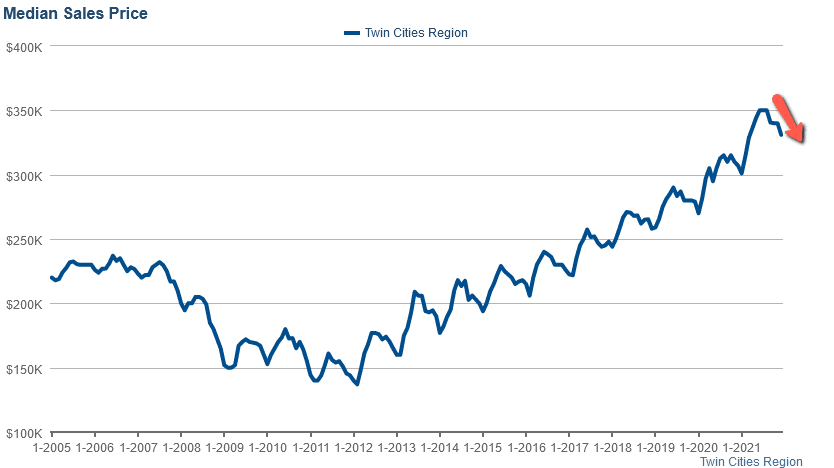

The Median Home Price: The median home price in the Twin Cities fell 2.6% in December to $331,000 as the seasonal contraction cycle continues. The median home price will probably fall marginally as a lagging indicator for sales closing in January as the demand in December was soft but with inventory bottoming and demand picking up in January, prices are likely to turn back up for sales that close in February.

Note: This doesn't mean that all home prices fell in December. There are some Twin Cities segments where prices continue to rise marginally through the winter contraction because inventory has fallen faster than demand or because the area has pent-up demand that remains unfulfilled.

The Median Home Price: The median home price in the Twin Cities fell 2.6% in December to $331,000 as the seasonal contraction cycle continues. The median home price will probably fall marginally as a lagging indicator for sales closing in January as the demand in December was soft but with inventory bottoming and demand picking up in January, prices are likely to turn back up for sales that close in February.

Note: This doesn't mean that all home prices fell in December. There are some Twin Cities segments where prices continue to rise marginally through the winter contraction because inventory has fallen faster than demand or because the area has pent-up demand that remains unfulfilled.

Home Inventory: Home inventory fell 32% in December to 4,287 units which is 20% below the previous all-time low in inventory that was set in December of 2020. This will set the stage for another significant rise in home prices in 2022. We expect another marginal dip in inventory in January and then we expect inventory to chase demand through late summer/early fall.

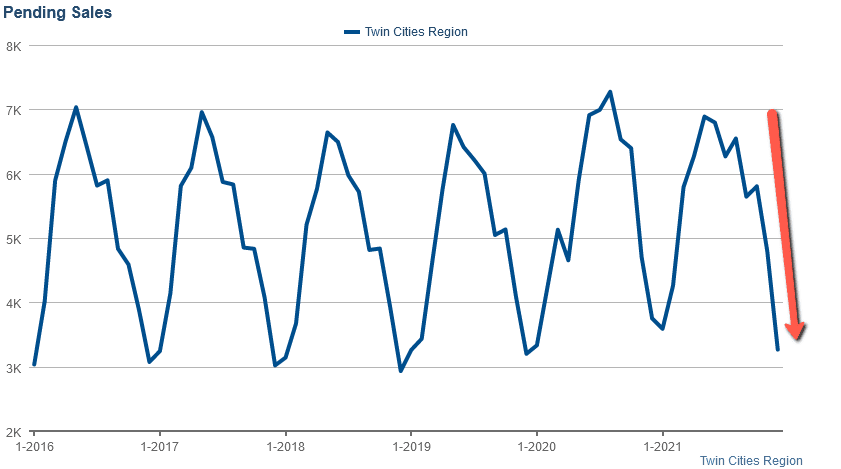

Pending Home Sales: Pending sales fell 31% in December to 3,265 units which is a predictable element of the seasonal contraction. We expect demand to move up marginally in January and then explode exponentially into the spring market of 2022.

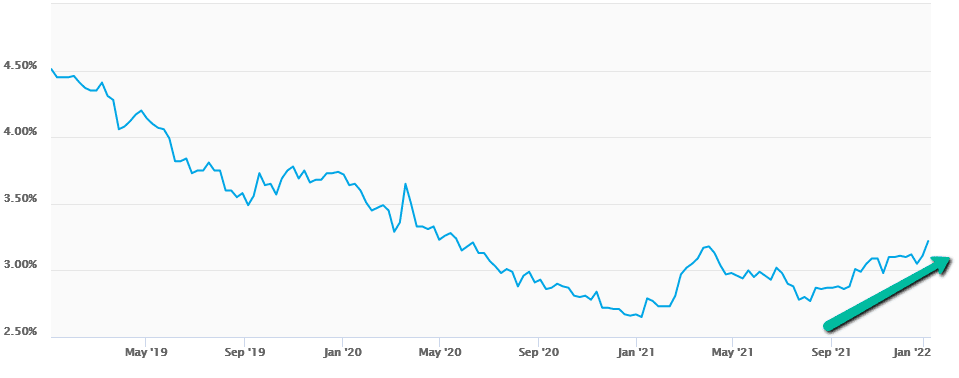

Mortgage Rates: Mortgage rates moved up 2.5% in December to 3.11% for the average 30-year-fixed conventional mortgage in the U.S. That rate is close to an 18-month-high but is still very low in historical terms.

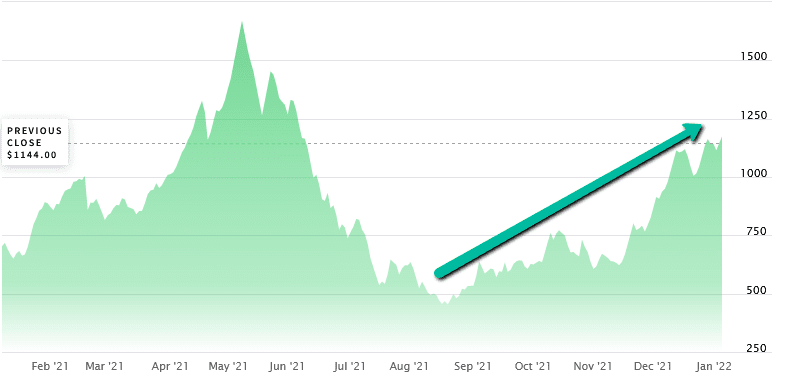

Lumber Prices: Lumber prices moved up another 20% in December. They remain up 126% from their correction in August and up 300% from their 2020 low.

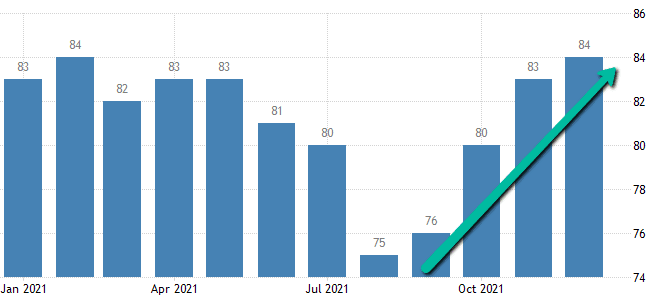

Home Builder Confidence: The NAHB housing market index in the US edged up 1 point to 84 in December of 2021, the highest since February and beating market forecasts of 83. Builders cited strong demand met with scarce inventory as their primary reasons for being optimistic.

This concludes my Twin Cities housing market insight for January of 2022. Please don't hesitate to call us at (952) 222-7653 if you would like to go more in-depth on a particular market segment or dive into the current fair market value of a property that you currently own or manage.